If your Social Security number has been flagged on the dark web, it means criminals now have one of the most powerful pieces of your identity, and they’re ready to use it. This guide explains exactly what that exposure means, how serious it is, and what you need to do today to protect yourself.

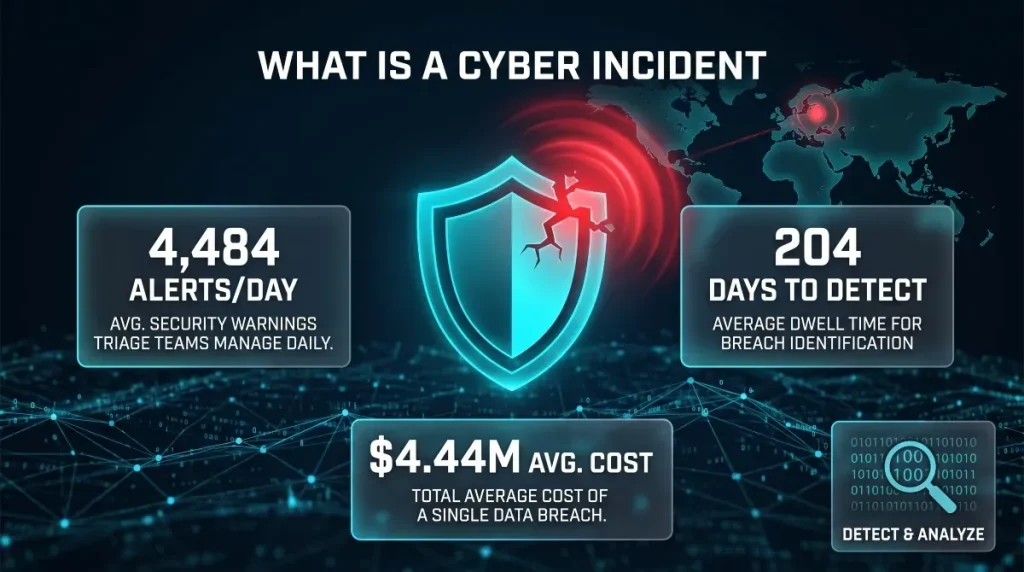

Your SSN doesn’t sit idle once it’s stolen. Dark web markets trade Social Security numbers alongside dates of birth, addresses, and financial account data in bundled “fullz” packages, complete identity kits sold to fraudsters for as little as $1 to $30. According to the Identity Theft Resource Center, over 422 million individuals were affected by data breaches in 2022 alone, with SSNs among the most frequently compromised data points. Once your number surfaces in one of these markets or paste sites, it can be resold, reused, and recycled across multiple fraud schemes for years.

The alert you received, whether from CreditWise, Discover, Experian, or another monitoring service, didn’t cause the problem. It surfaced one that already exists. What matters now isn’t panic. It’s a clear, fast response.

What Does It Mean When Your SSN Is Found on the Dark Web?

When your SSN is found on the dark web, it means your nine-digit identifier has been extracted from a data breach, malware infection, or phishing attack and is now available for purchase on criminal marketplaces. It does not mean your identity has already been stolen, but it does mean the window for misuse is open.

Your SSN is the master key to your financial identity. Unlike a compromised password or a stolen credit card number, you cannot reset it. A fraudster with your SSN can open new credit lines, file a tax return in your name, apply for government benefits, or build an entirely new synthetic identity, all without ever touching your existing accounts. The exposure itself is the risk, regardless of whether active fraud has started yet.

How Social Security Numbers End Up on Dark Web Markets

SSNs reach the dark web through a small number of well-established pathways. The most common are large-scale data breaches targeting healthcare providers, financial institutions, government contractors, and HR platforms, as well as organizations that collect SSNs for legitimate purposes and store them at scale. When those databases are compromised, millions of records move to dark web markets in bulk.

The second major pathway is infostealer malware. When a device is infected, often through a phishing email, a malicious download, or a compromised browser extension, the malware silently harvests saved credentials, autofill data, and documents stored locally. Tax returns, benefits letters, and onboarding documents frequently contain full SSNs and are exfiltrated into stealer logs, which are then sold on dark web Telegram channels and forums.

Phishing and social engineering round out the picture. Fraudsters impersonating the IRS, Social Security Administration, or financial institutions trick individuals into handing over their SSN directly. Once collected, those numbers are aggregated and listed for sale alongside other personal identifiers.

What Criminals Do With a Stolen SSN

A stolen SSN enables three primary fraud categories, each with distinct timelines and impact profiles.

Classic identity theft is the most immediate. A fraudster uses your SSN combined with your name, date of birth, and address to open new credit cards, take out personal loans, or drain financial accounts. This type of fraud typically surfaces within weeks and shows up on your credit report as unfamiliar accounts or hard inquiries.

Synthetic identity fraud is slower and harder to detect. Instead of impersonating you directly, criminals combine your real SSN with a fabricated name and address to create a new, fictional identity. They then spend months or years building credit under that synthetic profile before executing a large-scale “bust-out” fraud, maxing out credit lines and disappearing. Because the fraud isn’t attached to your name, standard credit monitoring often misses it entirely. The Federal Reserve has estimated that synthetic identity fraud costs U.S. lenders over $6 billion annually.

Tax refund fraud is a one-time but high-impact attack. A criminal files a tax return using your SSN before you do, claims a fraudulent refund, and collects it. You only discover the fraud when the IRS rejects your legitimate return as a duplicate. Resolution takes months and requires identity verification directly with the IRS.

SSN Found With Wrong Name: What Does That Mean

If a dark web alert shows your SSN paired with a name that isn’t yours, it isn’t a false alarm; it’s a signal of something more concerning. It most likely means your SSN is being used in a synthetic identity scheme, where your real number has been attached to a fabricated identity to build fraudulent credit.

It can also indicate a data entry error during a breach: your SSN was captured alongside someone else’s name because the source database had mismatched records. In either case, the underlying exposure is real. Your SSN is circulating, and whether or not the name attached to it matches yours, the risk of misuse remains the same. The wrong-name pairing simply adds a layer of complexity if you need to dispute fraudulent accounts later, since the fraud trail won’t directly match your identity on paper.

How Common Is This? The Scale of SSN Exposure

SSN exposure on the dark web is not rare; it is the expected outcome of participating in the modern financial system. Hundreds of millions of Social Security numbers have already been compromised through decades of data breaches, and the pace of new exposure is accelerating, not slowing.

How Many SSNs Are Currently on the Dark Web

The honest answer is: more than anyone can accurately count. Dark web markets, private Telegram channels, hacker forums, and paste sites collectively hold billions of stolen records, and SSNs appear in a significant portion of them. Researchers can measure the breach events that created that exposure.

The single largest known SSN exposure in history occurred in 2024, when a breach at National Public Data, a background check company, reportedly leaked approximately 2.9 billion records, including the Social Security numbers of nearly every living American adult. That one incident alone represents a near-total compromise of SSNs for the U.S. population at the data broker level.

That breach sits atop decades of accumulated exposure from healthcare providers, government agencies, financial institutions, and HR platforms. The cumulative picture is not reassuring: if you are an adult American who has ever applied for credit, filed taxes, received government benefits, or been employed, your SSN has almost certainly appeared in at least one compromised dataset.

Is Everyone’s SSN Already Out There?

Effectively, yes, for most American adults. Security researchers and identity protection professionals have largely shifted from asking “has my SSN been exposed?” to “is my SSN currently being actively misused?” That distinction matters because exposure alone does not guarantee fraud. It means the risk is persistent and ongoing, not hypothetical.

This doesn’t mean monitoring is pointless; it means monitoring becomes more critical, not less. Knowing when your SSN surfaces in a new breach, a fresh stealer log, or a dark web marketplace listing gives you a response window that unmonitored individuals simply don’t have. The difference between catching synthetic identity fraud early and discovering it years later, when your credit is destroyed, often comes down to whether you had visibility into dark web activity surrounding your data.

Which Data Breaches Have Exposed SSNs at Scale

Several landmark breaches have been responsible for the majority of SSN exposure currently circulating on the dark web.

The Office of Personnel Management (OPM) breach in 2015 exposed the SSNs and sensitive background investigation files of approximately 21.5 million current, former, and prospective federal employees and contractors, one of the most consequential government breaches in U.S. history.

The Equifax breach in 2017 compromised the personal data of 147 million Americans, including SSNs, dates of birth, addresses, and driver’s license numbers, pulled directly from one of the three agencies responsible for protecting financial identity.

Anthem Health (2015) exposed nearly 78.8 million records, including SSNs, from one of the largest health insurers in the country. Yahoo (2013–2014), Marriott (2018), and T-Mobile (multiple incidents between 2021 and 2023) collectively added tens of millions more compromised records to the dark web ecosystem.

The National Public Data breach in 2024 dwarfed all prior incidents in raw volume. Because NPD aggregated SSNs from public and private records at scale for background checks, the breach effectively distributed decades of compiled identity data to criminal actors in a single event.

These breaches don’t disappear after the news cycle ends. The records they produced continue to circulate, get repackaged, and resurface in new marketplaces years after the original incident, which is why a dark web alert today can trace back to a breach that happened a decade ago.

You Got an Alert: What the Notification Actually Means

A dark web alert telling you your SSN was found does not mean you’ve been hacked right now; it means a monitoring service has detected your Social Security number in a dataset on the dark web. The exposure likely predates the alert by weeks, months, or even years. The notification gives you a response window. How you use it determines what happens next.

CreditWise Dark Web Alert for SSN (Capital One)

CreditWise is Capital One’s free credit monitoring tool, available to anyone, not just Capital One customers. Its dark web monitoring feature scans for your SSN and email address across dark web sources and sends an alert when either appears in a detected dataset.

When CreditWise says your SSN is on the dark web, it has matched your number against a database of known compromised records. The alert is legitimate and worth taking seriously. However, CreditWise does not tell you which breach exposed your SSN, when the exposure occurred, or what other data was bundled with it. It confirms presence, not context.

Capital One’s own language in these alerts is appropriately cautious; it recommends reviewing your credit report and considering a fraud alert, but stops short of telling you that active fraud is occurring. That gap between “your SSN was found” and “here’s the full picture of your exposure” is where more comprehensive dark web monitoring becomes necessary.

Discover Dark Web Alert, SSN Found

Discover’s dark web monitoring is available to all Discover cardholders and scans for your SSN across thousands of dark web sites. When Discover sends an alert that your SSN was found on the dark web, the process is similar to CreditWise: your number has been matched against a database of known leaked data.

Discover’s alerts are generally reliable indicators of real exposure. The limitation is the same as most consumer-grade monitoring tools: the scan is reactive, not continuous. It detects your SSN in datasets that have already been indexed and catalogued, meaning freshly stolen data moving through private channels, closed Telegram groups, or new marketplace listings may not be captured immediately, if at all.

If you received a Discover dark web alert for your SSN, treat it as confirmed exposure and move directly to the response steps in this guide.

Experian Dark Web Alert, SSN Compromised

Experian’s dark web surveillance scans the dark web for your SSN as part of its IdentityWorks product, with a limited version available through its free membership tier. When Experian flags your SSN as compromised on the dark web, the alert carries particular weight, given Experian’s position as one of the three major credit bureaus, which has direct visibility into how your SSN is being used in the credit system alongside its dark web scanning function.

An Experian dark web alert for your SSN should be paired immediately with a review of your Experian credit report for unfamiliar accounts, hard inquiries, or address changes you didn’t initiate. Because Experian sits at the credit reporting layer, its alerts can sometimes be correlated with credit activity faster than third-party monitoring tools.

Limitation: Experian’s dark web scanning, like its competitors’, does not cover the full dark web ecosystem. Private forums, encrypted marketplaces, and stealer log channels that operate outside indexed dark web sources are not captured by standard consumer monitoring products.

IDNotify SSN Found on Dark Web

IDNotify is an identity protection service frequently bundled with TurboTax, TaxAct, and other financial software products. When IDNotify sends an alert that your SSN was found on the dark web, the detection is powered by third-party monitoring infrastructure that scans known dark web sources for your personal identifiers.

IDNotify alerts are typically triggered when a user’s SSN appears in a breach dataset or a dark web listing. The service provides additional context beyond basic alerts, including the type of information found and recommended next steps, but shares the same fundamental limitation as other consumer tools: it monitors only a subset of the dark web, not the full ecosystem.

One notable context for IDNotify alerts: because the service is frequently activated around tax season through software bundles, users often encounter their first-ever dark web SSN alert during that period. This is not coincidental; tax season is peak season for SSN-related fraud, and the timing of activating monitoring often coincides with when that fraud is most likely to be attempted.

Why These Alerts Fire, and What Their Limitations Are

Every consumer dark web monitoring service operates on the same basic model: they maintain or license a database of known compromised records collected from dark web sources, breach disclosures, and paste sites, then match your personal identifiers against that database. When a match is found, an alert fires.

That model has real value. It is also structurally limited in three important ways.

First, coverage is partial. No consumer monitoring tool scans the entire dark web. Private marketplaces, invite-only forums, encrypted channels, and freshly compiled stealer logs exist outside the indexed sources these tools rely on. Your SSN could be actively circulating in channels that consumer alerts will never detect.

Second, alerts are retrospective. By the time a breach dataset is indexed, catalogued, and matched against your profile, the data has often been available to criminals for weeks or months. The alert tells you what has already happened, not what is happening right now.

Third, alerts lack depth. Knowing your SSN was found is the starting point, not the full picture. Understanding which breach it came from, what other data was bundled with it, whether it has appeared in multiple sources, and whether it is actively being traded requires a level of threat intelligence that consumer-grade tools are not designed to provide.

This is the gap that purpose-built dark web monitoring platforms are designed to fill: continuous scanning across a broader source ecosystem, with context that moves beyond a simple match notification.

What Happens If Your SSN Is on the Dark Web?

Having your SSN on the dark web does not guarantee immediate fraud. Still, it creates a persistent, open-ended vulnerability that can be exploited at any point, days after the exposure or years later. The risk is not a single event. It is an ongoing condition that changes what you need to do to protect your financial identity in the future.

Short-Term Risks: Account Takeover and New Credit Lines

The most immediate threat following SSN exposure is new account fraud. A criminal with your SSN, combined with your name, date of birth, and address, all of which are typically bundled together in the same dark web dataset, has enough information to apply for credit cards, personal loans, auto financing, and utility accounts in your name.

This type of fraud can begin within days of a breach. The fraudster doesn’t need access to your existing bank accounts or passwords. Your SSN alone, paired with basic identity data, is sufficient to pass most standard credit application verification processes. According to Javelin Strategy & Research, new account fraud affected 3.2 million Americans in a single recent year, making it one of the fastest-growing categories of identity crime.

Account takeover, where a criminal uses your SSN alongside other data to reset account credentials or pass identity verification challenges, is a parallel risk. Financial institutions, telecom providers, and government portals frequently use SSNs as verification factors. Once a fraudster has it, those verification layers become entry points rather than barriers.

Long-Term Risks: Synthetic Identity Fraud and Tax Refund Theft

The more insidious risks from SSN exposure play out over months or years, often without any signal reaching you until significant damage is done.

Synthetic identity fraud is the slower burn. A criminal pairs your real SSN with a fabricated name, a manufactured address, and a new email to create a fictional identity. They then spend months building a credit profile under that synthetic persona, making small purchases, paying balances on time, and establishing tradelines. Once the credit profile is strong enough, they execute a bust-out: maxing every available credit line simultaneously and disappearing. Because the fraud was never committed in your name, it often doesn’t appear on your credit report directly. You may only discover it when a creditor eventually traces the SSN back to you and attempts to collect.

Tax refund fraud has an immediate impact but is equally difficult to detect before it happens. A fraudster files a federal or state tax return using your SSN before you do, claims a refund, and collects it, often via prepaid debit card or direct deposit to an account they control. When you file your legitimate return, the IRS rejects it as a duplicate submission. Resolving the dispute requires filing IRS Form 14039, verifying your identity directly with the agency, and waiting, a process that can take 6 months or more to resolve fully.

Both fraud types share the same feature: by the time you discover them, the damage is already done. Early detection through continuous dark web monitoring is the only reliable way to shorten that window.

Signs Your SSN Is Already Being Misused

In many cases, SSN misuse leaves a trail before the fraud becomes fully visible. Knowing what to look for can mean the difference between catching a problem early and discovering it after a fraudster has spent years building on your identity.

Unexplained hard inquiries on your credit report are often the first signal. If you see credit applications you don’t recognize, especially from lenders, auto dealers, or telecom providers, someone may be using your SSN to apply for new accounts. A hard inquiry you didn’t authorize is not a minor anomaly. It is a direct indicator that your SSN has been used in a credit application.

New accounts you didn’t open are the next stage. If unfamiliar credit cards, loans, or utility accounts appear on your credit report, SSN-based new account fraud is almost certainly underway. Similarly, collection notices for debts you don’t recognize, particularly from creditors you’ve never heard of, often indicate that a fraudulent account opened in your name has defaulted.

Other warning signs include your tax return being rejected by the IRS as a duplicate, receiving a benefits statement from the Social Security Administration that shows earnings from an employer you’ve never worked for, or getting medical bills for care you never received. Each of these indicates that your SSN is being actively used, either in a financial, employment, or healthcare fraud context.

If any of these signals appear, the response is not to wait and monitor. It is to act immediately, starting with the steps in the next section.

What to Do If Your SSN Is on the Dark Web, Step-by-Step

If your SSN has been found on the dark web, the right response is methodical, not panicked. The steps below represent the most effective sequence of actions to contain the damage, prevent new fraud, and establish ongoing protection, starting with the highest-impact actions first.

Step 1: Place a Credit Freeze With All Three Bureaus

A credit freeze is the single most effective protective action you can take after SSN exposure. It prevents any lender from accessing your credit file to approve new account applications, which means even a fraudster with your full identity cannot open a new credit account in your name while the freeze is active.

You must freeze your credit with each of the three major bureaus: Equifax, Experian, and TransUnion. Each bureau has its own online freeze portal, and the process takes approximately five minutes per bureau. Credit freezes are free by federal law, can be lifted temporarily when you need to apply for credit yourself, and have no negative impact on your credit score.

Do not rely on a fraud alert alone as a substitute. A freeze is a hard block. A fraud alert is a request that asks lenders to take extra verification steps, but does not prevent them from extending credit. If your SSN is confirmed on the dark web, a freeze is the appropriate level of protection.

If you have minor children, consider placing a freeze on their SSNs as well. Children’s SSNs are frequently targeted precisely because the fraud goes undetected for years, often not discovered until the child applies for their first credit card or student loan.

Step 2: Set Fraud Alerts (Initial vs. Extended)

A fraud alert is a notice placed on your credit file that instructs lenders to take additional steps to verify your identity before extending credit. It complements a credit freeze and covers scenarios where you temporarily lift the freeze for a legitimate credit application.

An initial fraud alert lasts one year and can be placed for free with any one of the three bureaus; that bureau is then required to notify the other two. It is appropriate if you have received a dark web alert but have not yet discovered active fraud.

An extended fraud alert lasts seven years and is available to confirmed victims of identity theft. It requires a copy of your FTC identity theft report (covered in Step 4) and provides a higher level of protection, including removal of your name from prescreened credit offer lists for five years.

Setting both a credit freeze and a fraud alert is not redundant; they operate at different layers of the credit application process and, together, create a stronger defensive posture than either alone.

Step 3: Check Your Credit Reports for Unauthorized Accounts

Once your freeze and fraud alert are in place, pull your full credit reports from all three bureaus and review them in detail. You are entitled to free weekly credit reports from each bureau at AnnualCreditReport.com, the only federally authorized source for free reports.

Look specifically for accounts you don’t recognize, hard inquiries from lenders you’ve never contacted, addresses you’ve never lived at, and employers you’ve never worked for. Any of these can indicate that your SSN has already been used to build a fraudulent credit profile.

If you find unauthorized accounts, do not simply dispute them online and move on. Document everything: the account name, the lender, the date it was opened, and the inquiry that preceded it. This documentation becomes essential if you need to file a police report or work through the FTC’s identity theft resolution process. The Consumer Financial Protection Bureau reports that identity theft complaints consistently rank among the top fraud categories reported to federal agencies each year, which means credit bureaus and lenders have established dispute processes. Still, those processes require evidence to move efficiently.

Step 4: File an Identity Theft Report (FTC + Police)

If you discover that your SSN has already been used to open accounts, file tax returns, or commit any form of fraud, filing an official identity theft report is a necessary step, not an optional one.

Start at IdentityTheft.gov, the FTC’s dedicated identity theft recovery platform. The site generates a personalized recovery plan and produces an official FTC Identity Theft Report, which is a legally recognized document that gives you specific rights: the ability to block fraudulent information from your credit reports, stop debt collectors from pursuing fraudulent debts, and obtain copies of documents related to the fraud.

A police report adds a layer of documentation, particularly useful when disputing accounts with lenders who require law enforcement involvement. Bring your FTC report, a government-issued ID, and any evidence of the fraudulent accounts to your local police department. Not every department will take an active investigative interest in identity theft, but the report itself is the asset, not the investigation.

Together, the FTC report and the police report constitute the evidence base you’ll need if the fraud escalates and requires legal dispute resolution.

Step 5: Secure Your Financial Accounts and Enable MFA

SSN exposure rarely travels alone. The same dataset that contains your Social Security number typically includes your name, date of birth, address, and sometimes your email address and phone number. That combination is sufficient for a fraudster to attempt to take over your existing financial accounts through social engineering, password reset flows, or identity verification challenges.

Log in to every financial account, bank, investment platforms, retirement accounts, credit cards, and take three immediate actions: change your password to a unique, strong credential generated by a password manager; enable multi-factor authentication using an authenticator app rather than SMS where possible; and review recent account activity for any transactions or access events you don’t recognize.

Contact your bank directly if you see anything suspicious. Financial institutions have fraud teams that can flag your account for enhanced monitoring and reverse unauthorized transactions faster than any dispute process. SMS-based two-factor authentication is better than nothing, but SIM swapping, where a fraudster convinces your carrier to transfer your phone number, is a known vector specifically used against people whose identity data is available on the dark web. An authenticator app eliminates that exposure.

Step 6: Monitor the Dark Web Continuously for New Exposure

Completing Steps 1 through 5 addresses the immediate threat. Step 6 is what prevents the next one.

A one-time dark web scan tells you about historical exposure. It cannot tell you when your SSN surfaces in a new breach next month, when a fresh stealer log containing your data gets published to a dark web forum, or when your credentials reappear in a newly compiled identity package being sold on a criminal marketplace. That requires continuous monitoring, not a snapshot.

Consumer alert services from CreditWise, Discover, or Experian provide a baseline, but as covered earlier in this guide, their coverage is partial, and their detection is retrospective. A purpose-built dark web monitoring platform scans a broader ecosystem of sources, including dark web markets, paste sites, stealer log repositories, and criminal forums. It surfaces new exposure as it happens rather than after it has been catalogued.

Run a free dark web report at dexpose.io/free-darkweb-report to see what’s currently exposed across your digital identity, beyond what standard consumer alerts cover. For ongoing protection, DeXpose’s continuous dark web monitoring tracks new exposure across markets, breach databases, and stealer logs, alerting you the moment your data surfaces so you can respond before fraud begins.

The steps above close the door on today’s exposure. Continuous monitoring ensures you’re not caught off guard when the next one opens.

Can You Remove Your SSN From the Dark Web?

You cannot remove your SSN from the dark web. Once your Social Security number has been published in a breach dataset, traded on a criminal marketplace, or posted to a paste site, that data exists across multiple servers, mirrors, and private archives that no individual, company, or government agency can fully reach or control.

Why Removal Is Not Possible, What Actually Works

The dark web is not a single database with an administrator who can process deletion requests. It is a decentralized network of hidden marketplaces, private forums, encrypted channels, and paste repositories, many of them operated anonymously across jurisdictions with no legal accountability to any authority. When a dataset containing your SSN is published, it is typically downloaded, copied, and redistributed within hours. By the time any monitoring service detects it, the data has already moved beyond any single point of origin.

Services that claim to “remove your information from the dark web” are misrepresenting what they do. What reputable services actually provide is suppression of your data from certain data broker sites on the surface web, combined with ongoing monitoring that alerts you when your information surfaces in new dark web sources. Those are genuinely useful functions, but they are categorically different from removal. The distinction matters because believing your SSN has been “removed” can create a false sense of security that leads you to skip the protective steps that actually work.

The actions that work are not removal-based. They are containment-based: freezing your credit so your SSN cannot be used to open new accounts, placing fraud alerts so lenders apply additional verification, monitoring your credit reports for unauthorized activity, and maintaining continuous visibility into new dark web exposure through active monitoring. These steps don’t erase the exposure; they neutralize its usefulness to criminals.

Mitigation vs. Monitoring: The Right Mindset

The most productive mental shift after SSN exposure is moving from a recovery mindset to a management mindset. Recovery implies a return to a prior state, your SSN back in your hands, the exposure undone. That state no longer exists. Management means accepting that your SSN is a permanently compromised identifier and building a protective posture designed for that reality.

This is not a counsel of despair. The majority of people whose SSNs are on the dark web never experience active fraud, not because exposure doesn’t matter, but because criminals are opportunistic and prioritize targets without protective measures in place. A credit freeze, active fraud alerts, and continuous dark web monitoring make you a significantly harder target than the tens of millions of exposed individuals who have taken no protective action at all.

The relevant question is no longer “how do I undo the exposure?” It is “how do I ensure that exposure never converts into fraud?” Mitigation partially and imperfectly answers the first question. Monitoring continuously answers the second question in real time.

How Dark Web Monitoring Gives You an Early Warning System

The core value of dark web monitoring after SSN exposure is time. Fraud, in almost every form, requires a window of undetected activity to cause meaningful damage. A fraudster opening a new credit line needs the account to age before executing a bust-out. A tax refund fraudster needs to file before you do. A synthetic identity builder needs months of credit activity before the profile is worth exploiting. Monitoring compresses the window between when your data is being actively used and when you find out about it.

A dark web monitoring platform that scans markets, stealer log repositories, paste sites, and criminal forums continuously, rather than matching against a static database of known historical breaches, can detect when your SSN appears in a freshly published dataset, a newly listed marketplace entry, or a stealer log from an infostealer campaign that concluded last week. That detection gap between “your data is being traded” and “you know about it” is where the majority of SSN-based fraud takes root.

For most people, the first warning they receive comes from a credit alert after fraud has already occurred, a new account has been opened, a hard inquiry has been recorded, or a collection notice has been generated. Dark web monitoring moves that alert upstream, to the moment of exposure rather than the moment of consequence. That shift from reactive to proactive is the difference between preventing fraud and recovering from it.

Get your free dark web report at dexpose.io/free-darkweb-report to see where your SSN and personal data currently appear across dark web sources, and set up continuous monitoring so you’re alerted the moment new exposure occurs.

How to Check If Your SSN Is on the Dark Web Right Now

The fastest way to check if your SSN is on the dark web is to run a dark web scan using a monitoring tool that searches beyond publicly known breach databases. Several options exist, ranging from free consumer tools to purpose-built threat intelligence platforms, and understanding what each one actually scans determines how much confidence you can place in the result.

Free Dark Web Scan Options (and Their Limitations)

The most widely used free dark web scanning tools include Have I Been Pwned (HIBP), Google One’s dark web report, CreditWise from Capital One, Experian’s free dark web scan, and Discover’s SSN monitoring for cardholders. Each of these provides genuine value as a starting point, and a positive result from any of them should be taken seriously.

Their shared limitation is architectural. Every consumer-grade free tool operates by matching your personal identifiers against a curated database of known breach data, records that have already been collected, processed, and indexed from publicly accessible dark web sources. That database is never complete, and it is always behind. It reflects what has already been discovered and catalogued, not what is currently circulating.

The dark web sources these tools don’t cover are often the most operationally relevant ones: private marketplaces that require vetted membership, closed Telegram channels where stealer logs are sold in bulk, newly compiled identity packages assembled from multiple breach sources, and paste sites that are scraped intermittently rather than monitored in real time. A clean result from a free scan does not mean your SSN is safe; it means your SSN wasn’t found in the subset of sources that the tool monitors. Those are meaningfully different statements.

Google discontinued its standalone Google One dark web report feature in 2024, migrating the functionality into Google One subscription tiers. For users who relied on it as a free, standalone tool, that coverage no longer exists in its prior form.

What DeXpose Scans That Free Tools Miss

DeXpose is built on a threat intelligence infrastructure designed for organizational dark web monitoring, which means its scanning depth operates at a categorically different level than consumer alert services.

Where free tools match against static or slowly updated breach databases, DeXpose continuously monitors live dark web sources: active marketplaces, stealer log repositories, criminal forums, Telegram channels, and paste site ecosystems. When a new stealer log is published containing credentials and identity data harvested from infected devices in the past week, DeXpose surfaces it. When your SSN appears in a freshly compiled identity package being listed on a dark web market today, DeXpose detects it. That real-time coverage is what transforms dark web monitoring from a historical snapshot into an actual early warning system.

DeXpose also provides context that free tools don’t. Rather than a binary “found / not found” alert, a DeXpose scan surfaces what data appeared alongside your SSN, whether it was bundled with passwords, financial account data, physical address history, or device credentials, giving you a clearer picture of the actual scope of your exposure and which protective actions are most urgently needed.

For individuals who have already received a dark web alert from CreditWise, Experian, or Discover, DeXpose functions as the next layer of investigation: not replacing the alert you received, but answering the questions it couldn’t.

Run Your Free DeXpose Dark Web Report

If your SSN has been flagged on the dark web, or if you simply haven’t checked and want to know what’s out there, the most actionable step you can take right now is running a free dark web report through DeXpose.

The report scans dark web markets, breach databases, stealer log sources, and paste sites for your exposed data, providing a clear picture of what’s currently circulating and where it originated. It takes less than a minute to run and requires no payment or credit card.

Run your free dark web report now at dexpose.io/free-darkweb-report. If continuous monitoring is what you need, ongoing alerts the moment your SSN or personal data surfaces in new dark web sources, DeXpose’s full dark web monitoring platform is available at dexpose.io/darkweb-breaches-monitoring.

The scan is free. The visibility it provides is not something a standard credit monitoring service offers.

How to Protect Your SSN in the Future

Protecting your SSN after dark web exposure is not about undoing the past; it is about making your number as difficult to exploit as possible going forward. The three habits below, practiced consistently, represent the most effective long-term defense available to any individual whose SSN is in circulation on the dark web.

Don’t Share Your SSN Unless Legally Required

The most underappreciated source of SSN exposure is not data breaches; it is unnecessary disclosure. Most requests for your Social Security number are optional, and most people comply without questioning whether it is actually required.

Your SSN is legally required in a narrow set of contexts: federal tax filings, employment eligibility verification (Form I-9), opening a bank account or investment account subject to federal reporting requirements, applying for federal benefits, and certain licensed financial transactions. Outside of these contexts, most requests for your SSN, from medical offices, landlords, utility providers, retailers offering store credit, and many others, are optional verification shortcuts, not legal mandates.

The practical habit is straightforward: when asked for your SSN, ask why it is needed and what the alternative is if you decline. Many organizations will accept alternative identifiers or simply proceed without them. Every unnecessary disclosure is a new exposure point, another database, another potential breach, another pathway to the dark web. Reducing the number of organizations that hold your SSN is the only way to reduce your long-term breach surface.

Freeze Your Credit as a Default Posture

Most people treat a credit freeze as an emergency response, something to activate after fraud occurs or an alert fires. The more protective posture is to keep your credit frozen by default and lift it only when you are actively applying for credit.

This represents a fundamental shift in how you think about your credit file. An unfrozen credit file is an open door. A frozen one requires a deliberate, authenticated action to open, an action that a fraudster cannot take without access to your bureau account credentials. Given that freezing costs nothing, the process takes minutes, and the freeze has no impact on your existing accounts or credit score, there is no meaningful downside to keeping it active permanently.

The friction of temporarily lifting a freeze, typically a five-minute online process with each bureau, is a far smaller inconvenience than resolving a fraudulent account. With SSNs now effectively permanent fixtures of the dark web ecosystem for most American adults, a default-frozen credit file is no longer overcautious. It is the rational baseline.

Use Continuous Dark Web Monitoring as Ongoing Protection

A one-time dark web scan tells you where your SSN stood at a single point in time. It cannot account for the breach that happens next month, the stealer log published next week, or the identity package compiled from multiple sources and listed on a dark web market tomorrow. Continuous monitoring is what converts a snapshot into an ongoing defensive posture.

The value of continuous monitoring compounds over time. Each new breach that exposes your SSN represents a fresh opportunity for fraud, with new criminals who now have your data, potentially bundled with updated information that makes it more actionable than older records. An early alert from a monitoring platform that detects your SSN in a new source gives you a response window. No alert means no window, and fraud proceeds go undetected until they surface in your credit report or on your tax return.

Javelin Strategy & Research found that identity theft victims with monitoring services in place experienced significantly lower out-of-pocket losses than those who discovered fraud through other means, primarily because early detection allows intervention before accounts are maxed out, debts are defaulted, or fraudulent returns are processed.

Set up continuous dark web monitoring through DeXpose at dexpose.io/darkweb-breaches-monitoring, or run a free initial scan at dexpose.io/free-darkweb-report to see your current exposure before activating ongoing protection. The goal is not to react to fraud after it happens. It is to ensure you know about new exposure before a fraudster has a chance to act on it.

Frequently Asked Questions (FAQ’s)

Is my SSN definitely being used if it’s on the dark web?

Not necessarily, dark web presence means your SSN is available for criminal use, not that active fraud has already begun. However, the risk is real and ongoing, which is why immediate protective action is essential, regardless of whether misuse has already begun.

Should I get a new Social Security number?

The SSA will issue a new SSN only in extreme, documented cases of ongoing harm, and even then, your old number doesn’t disappear from existing records, credit files, or criminal databases. A credit freeze and continuous dark web monitoring provide more practical protection than a new number in almost every real-world scenario.

How did my SSN end up on the dark web?

Your SSN most likely reached the dark web through a data breach at an organization that stored it, a healthcare provider, financial institution, employer, or data broker, or through infostealer malware that harvested documents from an infected device. Given the scale of breaches over the past decade, the source is often impossible to trace to a single incident.

What’s the difference between my SSN being “compromised” vs. “exposed”?

The terms are used interchangeably by most monitoring services, but technically, “exposed” refers to your SSN appearing in a leaked dataset, while “compromised” implies it has been accessed and is potentially being actively used. In practice, treat both alerts with equal urgency; the protective response is identical regardless of which term the notification uses.

Is CreditWise’s dark web SSN alert accurate?

CreditWise alerts are legitimate and based on real detections against known dark web datasets. If it fires, your SSN has genuinely appeared in a compromised source. The limitation is coverage depth, not accuracy; it confirms what it found, but cannot confirm what it didn’t scan.

My SSN was found under a different name. Is it still a threat?

Yes, a wrong name paired with your real SSN is a strong indicator of synthetic identity fraud, where your number is being used to build a fictional credit profile. The exposure is real, and the risk is active; the wrong name simply means the fraud trail won’t appear directly on your credit report, making it harder to detect without dedicated dark web monitoring.

How often does DeXpose scan for SSN exposure?

DeXpose monitors dark web sources continuously rather than on a fixed schedule, scanning active marketplaces, stealer log repositories, criminal forums, and paste sites in real time. When your SSN surfaces in a new source, you’re alerted immediately, not during the next scheduled scan cycle.